Millennials tend to have a dysfunctional relationship with investing. Many of us were just coming of age when the 2008 Recession hit full force, and this has resulted in a deep distrust of the stock market in many young adults. According to a 2014 study, only 46 percent of millennials have an investment account of any kind (IRA, 401(k), etc.). While a few more are saving some cash for retirement (55 percent), it seems that a combination of stock market mistrust, school loans and other debts, and a general lack of knowledge are keeping millennials from preparing for retirement in a meaningful way.

It’s not a good thing, but as a member of this generation, I know there’s a lot of time to turn things around. That’s what I want to talk about here. And it all starts with education. As soon as you start to understand how investment works, and how it is likely to impact your future, you’ll want to to start investing. I know this from personal experience. As a member of this generation, I know what it’s like to make these changes and start getting prepared for the future. But you’ve got to start from the beginning.

Why Invest at All?

Not a stupid question. I’m glad you asked. Money loses value over time. This is due to inflation. If you have $10,000 hidden under your mattress, it’s not going to have the same amount of buying power in 40 years when you take it out to pay for your retirement. Inflation is the reason that $1 no longer buys a gallon of gasoline. You’ve got to do something with your money to make it grow faster than the inflation rate. And that requires you to take a risk.

Risk is inherent in all forms of investment. In the 2008 Recession, and in the fallout of the recent stock market drop in China, a lot of people lost a lot of money. If you look at the stock market from the outside, it might seem like a giant random casino. But if you take a look at history, it’s got some important patterns that you can start to recognize. So, if you invest money in the stock market for decades, you have a very high probability of coming out with a lot more money than you started with. But, you’ve got to invest it the right way.

How Do You Invest in the Stock Market Without Losing Everything?

This is something that’s important to address. For people who don’t know a lot about the stock market, it’ll seem like some people win big while others lose it all, and that there’s not much you can do to prevent big setbacks. While there’s no risk-proof investment strategy, there are some approaches which are tried and true methods that have worked for millions of people. There are tons of ways to invest, but I’m going to outline a common “conservative” investment strategy that’s great for people who have never before invested for retirement.

When people succeed at stock market investment, it’s usually because they have diversified wisely. Diversification is built upon the knowledge that investing in just one or several stocks is likely to end in disaster. There are hundreds of factors that go into the value of individual stocks, and if you don’t spread out your risk, you’re likely to lose everything. Think of it like a bed of nails. You wouldn’t lay down on a bed made up of 10 nails. But if you make a bed of 500 or 1,000 nails, this lowers the risk factor considerably.

That’s where mutual funds come in. There are lots of different funds, but the ones I typically recommend to new investors are Index Mutual Funds. These funds are made up of lots of little bits of shares, taken from all the best performing stocks in individual markets. As individual stocks fall away, they’re replaced by new, better-performing stocks. ETFs are mutual funds traded just like stocks. They’re a little cheaper to trade, and they’re what I’ll recommend later on.

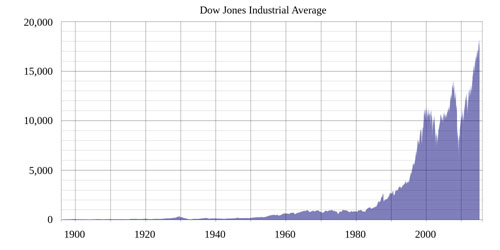

Index mutual funds tend to mirror the patterns of the overall markets they’re a part of. So if you started investing in IMFs in 1980, according to the chart above, you can see how many times over your initial investment would have grown. Of course, there are certain situations which don’t work out for investors, like people who invested in 2000, then divested themselves in 2009. But generally speaking, if you keep these funds active for decades, you will see big growth.

Plus, there are ways to insulate yourself as you get older. Say you are 24 years old, and you’re setting up your first investment account. You’ll have to decide how much of your investment money you want to put into stocks and bonds. Bond markets jump around a lot less than stocks, meaning there’s less risk and less reward. A strategy for many investors is to change their stock/bond allocation with time, putting more of their money into bonds. Bonds won’t provide much growth, but they’ll still beat inflation, thus preserving buying power, and they are extremely unlikely to result in a sudden loss of your money just before retirement.

So How Do I Do It?

The best way to get the process going is to take advantage of tax-sheltered investment accounts. If you have a job that offers a 401(k), you’ll want to be maxing that out every year, because your contributions are matched by your employer (free money). You should also create a Traditional or Roth IRA with a company such as Vanguard or Betterment (though there are many other options). You can check out the differences between those two accounts on your own time, but both are ways the government allows normal people to save for retirement without having to pay so much in taxes.

A company like Betterment is good for people who want a good range of ETFs picked out and organized for them. Go with Vanguard if you want to do-it-yourself and save a little money. But in either case, you’ll be able to easily start the process of meaningful retirement investment, and both sites will give you lots of resources to help you plan out your goals.

What Else Should I Know?

There’s no end to what can be learned about investment. But there are some important concepts to understand before you begin.

Compound interest: This is one of the coolest parts of investing. As you invest, you earn interest. That interest can be added to the investment pot and earn its own interest. The longer you do this, the faster your investments grow. It’s been called the most powerful force in investing.

‘Buy and hold’: If you follow investment media, you know that analysts and reporters love to freak out over changes to the stock market. Don’t listen to them. If you adopt the strategy I’ve laid out above, your investment is almost sure to survive the occasional drops that always happen in investing. Just remember that, historically, the market grows more than it declines. It is very likely to continue this trend during your lifetime.

Contributions: Of course, you’re not just going to invest a lump sum and let it sit for the next 40 years. You’re going to make regular contributions to combine with the interest and dividends you’re earning from your initial investment. Tax sheltered investment accounts have yearly maximum contribution amounts.

Predicting the market: Danger! Danger! Lots of writers and thinkers have concluded that economic markets are way too complicated for any one person to comprehend. People will sometimes recommend buying and selling stocks all the time to try to take advantage of high and low points. This isn’t recommended and frequently turns sound investment strategy into pure gambling.

Anything Else?

I could talk about beginning investment forever, but this is a good place to start. If you have questions or comments, write them down below and I’ll address them in a future post. Generally speaking, retirement investment isn’t rocket science. If you’re a young adult, you’ve probably still got plenty of time to get the ball rolling with retirement investment. Start now, do a little research and you’ll start to see your future look a whole lot more secure. The strategy I mapped out above is likely to work out over years and decades, so if you do nothing else, I recommend you start investing this way today.

•How to Start Investing and Why Now Is a Good Time to Do It

•Path to Early Retirement

•Motif Review

Leave a Reply